Mega Growth vs. Venture at Scale Deals

As venture backed companies stay private for longer and IPO activity remains low, a new class of private companies are raising funds at $10B+ valuations.

At first glance, it may be easy to believe that companies raising at decacorn-plus prices from a similar group of funds share similar stages and risk profiles. However, in the age of gen AI, price is not always a strong indicator for company stage, and growth stage prices do not always mean growth stage risk. I like to make the distinction between Mega Growth and Venture at Scale deals. They are vastly different in many ways – most importantly in the maturity and risk profiles of companies. Let’s jump into some of these key differences.

Key Differences

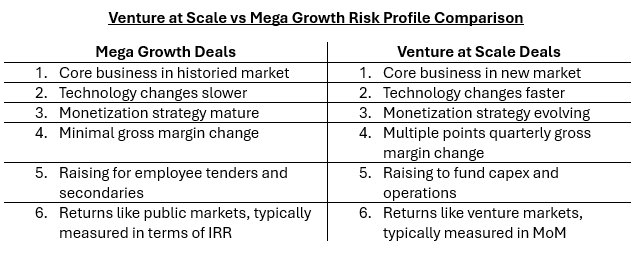

1. Core Market

Mega Growth and Venture at Scale deals provide exposure to end markets with different levels of maturity. Mega Growth deal businesses frequently have a core in a more mature end market. As an investor, you need to underwrite continued success in an existing market. Venture at Scale deals frequently give exposure to less mature end markets, such as consumer gen AI. This is a ~2 years old industry with emerging use cases and a rapidly evolving competitive landscape.

2. Product and/or Technology

Mega Growth stage companies typically have at least one core product built on well-established technologies. For example, a payment gateway API built on known payment protocols. These companies may have “Act III” products using more frontier tech, but the core product and technology remains proven. Venture at Scale companies are still building their “Act I” products, and these products tend to be based on technologies that are still seeing material improvements every few months.

3. Monetization Strategy

Mega Growth and Venture at Scale companies are at different points in their monetization journey. A Mega Growth deal involves companies that have well-defined monetization strategies that have been in play for many years. In comparison, Venture at Growth companies are often still experimenting with different monetization strategies. They may be changing prices, adding new pricing tiers, or rolling out new monetization strategies every few months.

4. Gross Margin Profile

A sub-point to monetization is gross margin. Mega Growth deals involve companies with fairly consistent gross margins. Investors typically do not underwrite 5ppt+ improvement in gross margins for a product line. In comparison, Venture at Scale deals can involve companies with quickly evolving gross margins. They may be changing a couple ppts every quarter. Companies may also reclassify what is included above or below gross margin.

5. Use of Proceeds

Mega Growth and Venture at Scale deal proceeds typically go towards different use cases. Mega Growth companies frequently have majority of operating cash flow needs covered, and may be raising billion of dollars for employee tenders, tax coverage, or secondary sales. Venture at Scale deals raise large rounds partially because these companies tend to have more capital intensive business models. Their proceeds tend to go towards capex investments and standard operating expense needs.

6. Return Expectations

Due to these differences in company maturity and risk profile, the smart investor will want different levels of returns for these investments. For Mega Growth deals where businesses are more derisked, investors typically underwrite to a certain IRR profile. Oftentimes they may be expecting an IPO in less than 5 year’s time. An investment in a Mega Growth deal is in many ways a bet that this company will continue to do what it is already doing, and investors are looking for public market level returns.

In comparison, for a Venture at Scale deal where the company is much riskier, investors should be underwriting to venture-like MoM outcomes. However, investors may be willing to reduce the discount rate and accept a lower MoM threshold for a few reasons:

They believe the market opportunity is incredibly large – any company with any type of success in this market will be worth far more than what they are paying today.

They believe that the founding team is particularly special.

So the multi-billion dollar price is less a reflection of the maturity of the company and more based on the size of the market opportunity and/or a vote of confidence in the founding team.

Example Deals

Let’s use a few examples to highlight the differences between Mega Growth and Venture at Scale Deals. Databricks’ $10B raise at $62B valuation is a great example of a Mega Growth deal.

Databricks’ core end market is enterprise cloud data infrastructure. This is a multi-decades old industry with fairly mature public companies (ex: Amazon Web Services, Snowflake) and well-defined use cases (ex: revenue forecasting, predictive modeling). They already built out two key product segments for this market – Spark compute and lakehouse – which make a strong core business on their own. Gen AI is their Act III.

Databricks’ core Spark architecture and lakehouse platform are tried-and-true technologies. The underlying Spark technology is not undergoing step change improvements every few months today.

Databricks’ monetization strategy is well-defined. Databricks has been doing usage-based monetization for over a decade now.

Databricks’ gross margin profile has been very consistent with limited change in recent years.

They need to raise billions of dollars to do an employee tender and pay taxes owed on stock buybacks. This is effectively a secondaries transaction to support employee liquidity

Investors are comparing returns for an investment in Databricks to holding public comps, such as Snowflake.

Meanwhile, xAI’s $6B fundraise at $50B post valuation is a great example of a venture at scale deal.

xAI’s core market today is consumer gen AI. This is a ~2 years old industry with emerging use cases and a quickly evolving competitive landscape.

Foundation model technology is still changing rapidly – we see step-change improvements with new models launched every few months.

xAI’s monetization strategy is evolving. Today, they receive a portion of X.com (fka Twitter) premium subscription revenue. This could change if xAI launches a standalone app, or integrates with Tesla cars.

Unknown.

News outlets speculate this fundraise will primarily be used for buying Nvidia chips.

Most importantly, Elon is a special founder. In the case of xAI, he is the biggest driver for why the company is valued at $50B.

Conclusion

To summarize, both Mega Growth and Venture at Scale deals provide opportunities to deploy multi-hundred-dollar checks at multi-billion-dollar valuations. And they frequently attract similar investors. But they represent fundamentally distinct bets with very different risk / reward profiles. While Mega Growth deals are about continued momentum in proven markets with returns comped to public markets, Venture at Scale deals are often bold wagers on nascent markets, new technologies, and exceptional founders. For investors, knowing what game you are playing isn’t optional — it is critical for portfolio construction and ultimately winning.

Special thank you to for ideas and feedback.

Sources: TechCrunch, CNBC, Bloomberg

Disclaimers: The information presented in this newsletter is the opinion of the author and does not necessarily reflect the view of any other person or entity, including Altimeter Capital Management, LP ("Altimeter"). The information provided is believed to be from reliable sources but no liability is accepted for any inaccuracies. This is for information purposes and should not be construed as an investment recommendation. Past performance is no guarantee of future performance. Altimeter is an investment adviser registered with the U.S. Securities and Exchange Commission. Registration does not imply a certain level of skill or training.

This post and the information presented are intended for informational purposes only. The views expressed herein are the author’s alone and do not constitute an offer to sell, or a recommendation to purchase, or a solicitation of an offer to buy, any security, nor a recommendation for any investment product or service. While certain information contained herein has been obtained from sources believed to be reliable, neither the author nor any of his employers or their affiliates have independently verified this information, and its accuracy and completeness cannot be guaranteed. Accordingly, no representation or warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, timeliness or completeness of this information. The author and all employers and their affiliated persons assume no liability for this information and no obligation to update the information or analysis contained herein in the future.

Great piece. Would be interesting to dive a bit deeper into more ‘venture at scale’ examples. It seems the pricing for these companies is still too rich to deliver the commensurate risk-adjusted returns. Another interesting analysis would be the category of companies who are between Act I and Act III - core business proven with great margins, but expansion is not yet proven. This is still a bit riskier than the company embarking on its third act as they’ve already proven they can rearchitect their GTM (around platformisation) compared to the company doing it for the first time.